Statutory Accounts Preparation Guide for UK Businesses

- KeystoneFA

- 3 days ago

- 8 min read

Statutory accounts preparation is the process of compiling your company’s financial records into official documents required by UK law for annual filing with Companies House and HMRC. All UK limited companies must prepare statutory accounts, even if dormant, making this a non-negotiable compliance requirement. The process covers everything from gathering bank statements and payroll summaries to drafting a balance sheet under FRS 102 or FRS 105. This statutory accounts preparation guide walks you through every stage, including the critical 2026 change that ended Companies House direct online filing and now requires commercial software for all submissions.

What documents do you need before preparing statutory accounts?

Gathering the right records before you start is the single biggest factor in how smooth your preparation runs. Missing one document at the draft stage can delay filing by weeks and trigger unnecessary accountant queries.

The core documents you need fall into five categories:

Document type | Purpose |

Bank, merchant, and loan statements | Reconcile all cash movements and outstanding balances at year end |

Sales records and unpaid invoices | Confirm revenue and trade debtors on the balance sheet |

Supplier bills and creditor balances | Verify trade creditors and accrued expenses |

Stock valuations and asset invoices | Support inventory figures and fixed asset additions |

Payroll summaries and dividend records | Confirm staff costs, PAYE liabilities, and director distributions |

Complete financial records also include related party transaction details, loan agreements between directors and the company, and any hire purchase or lease contracts. These disclosures are legally required in the notes to your accounts. Skipping them is one of the most common reasons accounts get rejected or queried.

For format, provide bank statements in CSV or Excel where possible, and PDFs as a backup. Your accountant can process structured data far faster than scanned paper copies. If you use Xero, QuickBooks, or Sage, export your trial balance and transaction reports directly from the software before your year end date.

Pro Tip: Create a shared folder labeled by tax year and drop documents in throughout the year. By the time your accountant asks for records, you will have 80% of the work already done.

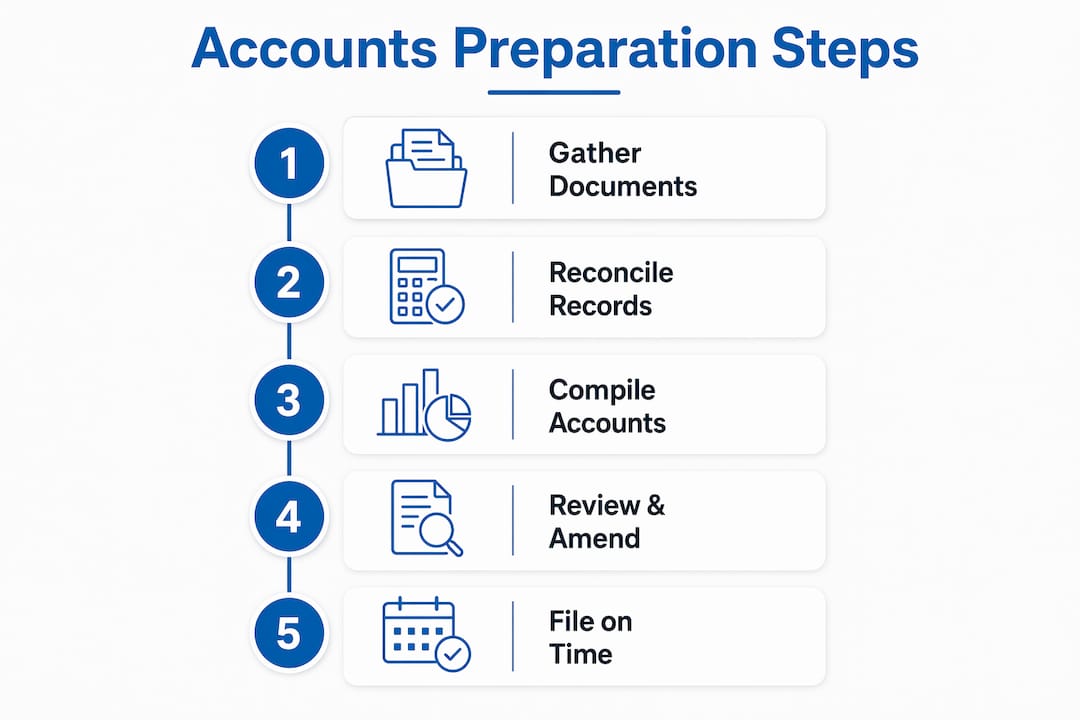

How to prepare statutory accounts: a step-by-step process

The actual preparation of statutory financial statements follows a defined sequence. Skipping steps or doing them out of order creates errors that compound later in the process.

Reconcile all accounts at year end. Match every bank, merchant account (Stripe, PayPal, Square), and loan balance to your accounting software. Timing differences in payroll and VAT are the most frequent source of discrepancies.

Verify trade debtors and creditors. Run an aged debtors report and confirm which invoices were genuinely outstanding at year end. Do the same for supplier balances. Write off any bad debts that are irrecoverable before finalizing figures.

Count and value inventory. Stock must be valued at the lower of cost or net realizable value under UK GAAP. If you hold physical stock, a year-end count is required. Overvaluing inventory inflates profit and creates a tax liability you have not earned.

Post accruals and prepayments. Accruals capture costs incurred but not yet invoiced, such as utility bills or professional fees. Prepayments reverse costs paid in advance that relate to the next period. Both adjustments are required to show a true and fair view.

Calculate and post depreciation. Fixed assets must be depreciated over their useful economic life. The method (straight-line or reducing balance) must be consistent year on year and disclosed in the accounting policies note.

Draft the balance sheet and profit and loss account. Year-end accounts must comply with UK GAAP, specifically FRS 102 for most companies or FRS 105 for micro-entities. The accounts must present a true and fair view and comply with the Companies Act 2006.

Prepare the notes to the accounts. Notes must cover accounting policies, related party transactions, contingent liabilities, going concern assessment, and director remuneration. These are not optional extras. They are part of the statutory document.

Tie figures to the corporation tax computation. Your accountant will adjust accounting profit for tax purposes. Confirming that the two sets of figures reconcile before submission prevents HMRC queries later.

Apply iXBRL tagging and file. iXBRL tagging is required for electronic submission. The software packages your accounts in a ZIP file that meets Companies House technical requirements.

Pro Tip: Start your reconciliation 2–4 weeks before your year end date. Early preparation gives you time to spot tax planning opportunities like pension contributions or dividend timing before the window closes.

What are the most common mistakes in statutory accounts preparation?

Most errors in preparing company accounts are not complex accounting failures. They are process failures that a bit of discipline would prevent.

The most damaging mistake is ignoring timing differences in payroll and VAT reconciliations. A payroll run processed on April 5 but relating to March will sit in the wrong period unless you adjust for it. Data integrity requires active human oversight beyond what any software export can provide. Cloud accounting tools like Xero and QuickBooks automate a great deal, but they cannot decide whether a transaction belongs in this period or the next.

The second most common error is misclassifying expenses or assets. Buying a laptop is a capital expenditure, not an office supplies cost. Treating it as revenue expenditure understates your asset base and distorts your profit figure. HMRC notices these patterns, particularly in companies with high equipment spend.

Overlooking related party transactions is a legal compliance failure, not just an accounting error. If a director lends money to the company or a connected party provides services, those transactions must be disclosed in the notes. Omitting them can expose directors to personal liability.

Critical warning: Missing your Companies House filing deadline triggers automatic penalties starting at £150 for private companies and rising to £1,500 for accounts more than six months late. Repeat late filing doubles the penalty. Filing on time is not optional, and HMRC penalties for late corporation tax returns add a separate layer of risk.

Pro Tip: Set a calendar reminder three months before your filing deadline. That gives you enough time to gather records, resolve queries, and still file early if everything goes smoothly.

How do you file statutory accounts after the 2026 Companies House changes?

The Companies House online filing service closed on March 31, 2026. Every UK company must now use commercial software to file statutory accounts. This is not a temporary measure. It is a permanent shift in how the UK government processes company filings.

The software you use must support iXBRL tagging and produce a ZIP file in the format Companies House accepts. The most widely used options in the UK market include Xero, Sage, QuickBooks, and specialist filing tools like Taxfiler, IRIS, and Digita. Your choice depends on company size and whether you are filing yourself or through an accountant.

Filing requirements differ by company size:

Micro-entities (turnover under £632,000, balance sheet under £316,000, fewer than 10 employees): can file abridged accounts using FRS 105, with minimal disclosure requirements.

Small companies (turnover under £10.2 million, balance sheet under £5.1 million, fewer than 50 employees): can file abridged or full accounts under FRS 102 Section 1A.

Medium and large companies: must file full statutory accounts including a directors’ report, strategic report, and audited financial statements where applicable.

The filing deadline for private limited companies is nine months after the accounting reference date. For public companies, it is six months. Missing these deadlines triggers the penalty structure described above.

Working with a qualified accountant who uses compliant software removes the technical burden from you entirely. KeystoneFA uses current iXBRL-compliant tools and handles the full filing process for clients, so you never have to navigate the technical requirements yourself. You can explore accounting services for UK businesses to understand what full-service support looks like in practice.

Key Takeaways

Preparing statutory accounts correctly requires structured document gathering, disciplined reconciliation, and compliant software filing under the UK’s 2026 rules.

Point | Details |

All UK companies must file | Even dormant companies must prepare statutory accounts and file with Companies House annually. |

Document gathering comes first | Collect bank statements, payroll summaries, stock valuations, and related party records before starting. |

Follow a defined preparation sequence | Reconcile, verify debtors and creditors, post accruals, calculate depreciation, then draft accounts. |

Commercial software is now mandatory | The Companies House online filing service closed March 31, 2026; iXBRL-compliant software is required. |

Start early to avoid penalties | Beginning 2–4 weeks before year end creates space for tax planning and prevents last-minute errors. |

Why I treat statutory accounts as a year-round discipline, not a year-end task

Most business owners I work with treat statutory accounts preparation the same way they treat a dental appointment: something to endure once a year and forget about until the next reminder. That mindset is the root cause of most of the problems I see.

The companies that consistently file clean, penalty-free accounts are the ones where the director or financial manager has kept their bookkeeping current throughout the year. They reconcile monthly. They flag unusual transactions when they happen, not six months later when no one remembers the context. By the time their year end arrives, the accounts are 80% done.

The companies that struggle are the ones who hand over a box of receipts in month ten and expect a miracle. Software like Xero or QuickBooks helps enormously, but it does not replace judgment. A bank feed import does not know whether a payment to a director is a salary, a loan, or a dividend. A human does.

One thing I have seen consistently with UK SMEs is that early preparation creates tax planning opportunities that late preparation destroys. Starting 2–4 weeks before year end gives you time to make a pension contribution, time a dividend, or accelerate a capital purchase before the window closes. Those decisions can save thousands of pounds. You cannot make them after the year end date has passed.

My honest advice: treat your accounts like a live document, not an annual event. The cost of getting it wrong, in penalties, HMRC queries, and accountant time, is always higher than the cost of staying organized.

— Shoaib

How KeystoneFA supports your statutory accounts and compliance

KeystoneFA works with founders, growing businesses, and financial managers across the UK to handle the full statutory accounts process, from document gathering to iXBRL-compliant filing with Companies House and HMRC.

The team at KeystoneFA uses current compliant software and brings direct experience from top UK and Middle East accounting firms. Whether you need support with year-end accounts, corporation tax, or a tax consultation to optimize your position before filing, KeystoneFA provides the kind of personalized attention that larger firms rarely offer. You get a named advisor who understands your business, not a rotating team of generalists. Book a consultation to get started with a team that treats your compliance as seriously as you do.

FAQ

What are statutory accounts?

Statutory accounts are the official annual financial statements that UK limited companies must prepare and file with Companies House and HMRC. They include a balance sheet, profit and loss account, and supporting notes.

Do small businesses need to prepare full statutory accounts?

Small and micro-entities can file simplified or abridged accounts with Companies House, but they must still prepare full accounts for their own records and for HMRC corporation tax purposes.

What software do I need to file statutory accounts in 2026?

The Companies House direct online filing service closed on March 31, 2026. You now need commercial iXBRL-compliant software such as Xero, Sage, IRIS, or Taxfiler to submit statutory accounts electronically.

What is the filing deadline for statutory accounts?

Private limited companies must file their statutory accounts within nine months of their accounting reference date. Missing this deadline triggers automatic financial penalties that increase the longer the accounts remain outstanding.

What happens if statutory accounts contain errors?

Errors in filed accounts can trigger HMRC inquiries, Companies House rejection, and potential director liability, particularly if related party transactions or director loans are misreported or omitted from the notes.

Recommended